Page Content

New series answers your questions about the Alberta Teachers’ Pension Plan

We’ve all heard the pension plan rhetoric: that defined benefit pension plans, like the one paid into by Alberta teachers, provide public sector workers with gold-plated pensions on the backs of taxpayers. On the other hand, banks and investment companies cause us to worry about how we’re going to make ends meet during our retirement by routinely suggesting that retiring comfortably requires a huge nest egg, usually in the millions of dollars.

In the midst of all this pension envy and retirement angst, teachers look at the amount of pension contributions they’re making every month and wonder if they’ll get back what they’ve paid in.

To answer these questions the Alberta Teachers’ Association has launched My Pension, My Future, a campaign to provide teachers with information about the Alberta Teachers’ Pension Plan, the benefits they will receive and the value of their investment. During this school year, the ATA News will feature a series of articles explaining different aspects of the plan. Also look for the My Pension, My Future postcards coming in the ATA school mailing.

What’s in it for me?

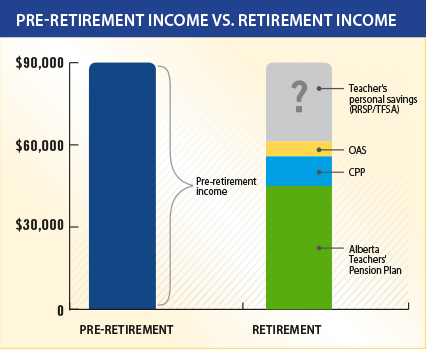

Teachers ask the question when they think about retirement, “What pension will I receive and how does this compare to retirement income streams available to other Canadian workers?”

Teachers have potentially three sources of retirement income:

- Government retirement income plans such as the Canada Pension Plan (CPP) and Old Age Security (OAS),

- Private employment pension plans such as our Alberta Teachers’ Pension Plan, and

- Individual savings such as registered retirement savings plans (RRSPs) or tax-free savings accounts (TFSAs).

Pillar 1: Government plans

Like all other Canadians who have CPP deducted from their paycheques during their working years, teachers are eligible for Canada Pension Plan payments at age 65. CPP is a pension plan funded and invested much like our teachers’ plan, with equal contributions from employers and employees. Most teachers with 30 years of full-time service will qualify for the maximum CPP, which is $1,038.33 per month and will likely also qualify for OAS, which has a maximum payout of $558.71 per month.

OAS is not a separate pension fund like CPP but rather the payments come from general government coffers, and the benefit is based on length of Canadian residency and is income tested.

Canada, like other countries in the world, is gradually increasing the age at which a citizen can access OAS to age 67, but this change won’t affect those born before 1958. For a teacher earning $90,000 a year prior to retirement, the government retirement income programs could replace approximately 18 per cent of their pre-retirement income.

Pillar 2: Alberta Teachers’ Pension Plan

Alberta teachers are part of the 38.4 per cent of Canadians who belong to a registered pension plan (Statistics Canada 2011). Teachers who retire at age 65 with 30 years of service can receive approximately 50 per cent of their pre-retirement income, although this number may be less if the pension is shared with a spouse or pension partner.

Pillar 3: Personal savings

There are two financial vehicles that provide tax benefits that are available to teachers (and other Canadians) to save for retirement: RRSPs and TFSAs. RRSP contributions are limited by the Income Tax Act and provide a tax benefit in the working year but are taxable after funds are withdrawn. A TFSA, on the other hand, receives no tax benefit up front, but remains tax free as it grows and its funds are withdrawn. The benefit from the teachers’ pension plan does take up RRSP room, but generally teachers do still have some ability to contribute. TFSAs are not linked to RRSP room or the pension plan benefit.

Together, the government retirement income plans and the teachers’ pension plan will replace approximately 70 per cent of a teacher’s pre-retirement income after 30 years of service. Personal savings is the variable that can increase that retirement income. ❚

For more information on pension amounts, see www.ATRF.com. Information about CPP and OAS can be found at www.servicecanada.gc.ca, and information on saving for retirement and the ATA group RRSP is available at www.capitalestateplanning.com. Retirement and pension information on various topics can also be found on the ATA website.