Page Content

With another fiscal crisis on its hands, what can the province do?

Analysis

Once again a dramatic drop in energy prices has the provincial government facing another fiscal crisis. There is talk of deficits, expenditure cuts and even tax increases. Everything is open for consideration. How large is the problem and how do alternative “solutions” compare?

Once again a dramatic drop in energy prices has the provincial government facing another fiscal crisis. There is talk of deficits, expenditure cuts and even tax increases. Everything is open for consideration. How large is the problem and how do alternative “solutions” compare?

How big is the problem?

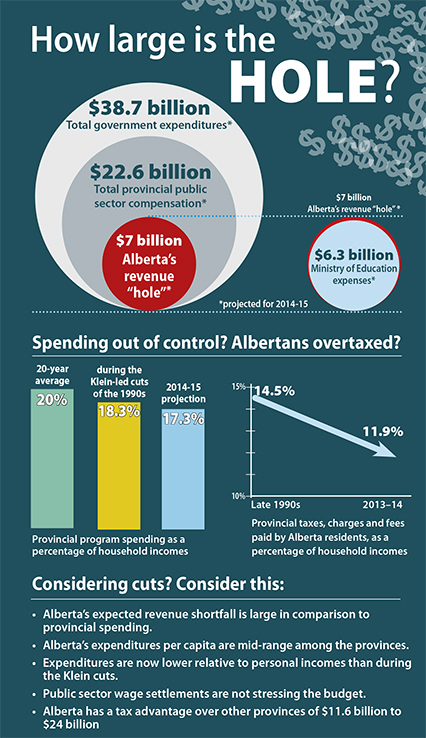

The recent collapse in oil prices is projected to result in a $7 billion reduction in provincial government revenues. That amount is 15.8 per cent of the total revenues expected in fiscal 2014–15 and could leave the province with a $5 billion operating deficit in 2015–16. That’s if we’re fortunate.

Regrettably, the province’s fiscal situation is actually worse than these numbers suggest. For several years the province has been borrowing to finance part of its capital expenditures —Budget 2014 projected $4.9 billion of direct borrowing in 2014–15 and a total of $21.6 billion of capital financing debt accumulating by the end of 2016–17 (even when the price of oil was expected to be $95 U.S.).

That is, despite the positive projections in Budget 2014, Alberta faced a structural deficit. Although estimates are tenuous, it may be reasonable to estimate that $4 billion of additional revenue is needed annually to meet planned infrastructure outlays so as to avoid borrowing and accumulating debt. Thus, a conservative estimate of the total amount needed to balance the budget in full is $9 billion. That is 20 per cent of the revenue initially projected for 2014–15 and 35 per cent of the revenue the province now generates from setting tax rates and charges.

Deficits?

How might the province address the looming gap between revenues and expenditures? A short-term measure is to run a (larger) deficit. Faced with a recession, this can be good counter-cyclical policy. Deficit spending will support employment and the economy during an economic downturn and enable the provincial and municipal governments to acquire some relatively lower-cost infrastructure. But more deficit spending is only a temporary measure, and we should expect to achieve balanced budgets soon, even if oil prices do not recover to $95 a barrel. The province has a $5 billion contingency account that could help finance a deficit for a year or so.

Spending cuts?

As Albertans try to balance the budget in a low oil price environment, there will be calls for decreased provincial spending. Whatever the revenue deficiency number used, the expenditure cut to offset it is large. For example, a $7 billion revenue “hole” is larger than the Ministry of Education’s outlays or larger than the budgeted capital spending. This $7 billion is also about 31 per cent of total provincial public sector compensation. More broadly, a $5 billion operating deficit is 12.4 per cent of operating expenditures, $7 billion is 17.3 per cent of operating outlays, and the $9 billion needed to cover the true deficit is 19.1 per cent of total expenditures (operating plus capital).

Cuts of these magnitudes are reminiscent of the spending cuts spearheaded by Ralph Klein in the 1990s, cuts that were unsustainable and debilitated infrastructure. The Klein cuts temporarily reduced provincial program expenditures to about 18.3 per cent of household incomes. Program expenditures in 2014–15 are even now estimated to be 17.3 per cent of household incomes and well below the 20 per cent level they have averaged over the previous 20 years. The current policy of restraining provincial expenditure increases to less than the inflation rate plus the population growth rate will drive the level even lower and further into yet unexperienced levels.

Despite the rapid growth and relative prosperity, Alberta is not a high per capita expenditure province. Even in 2013–14, with program expenditures inflated by flood recovery, Alberta ranked third largest in per capita expenditures. In 2014–15, it is projected to rank sixth. Essentially, program spending is only lower per capita in B.C. and Ontario (the only two provinces really below the average). Even there, because of the relatively larger role of local governments in those provinces, the differences in the consolidated provincial and local per capita expenditures are narrower than the provincial numbers alone suggest.

Finally, while public sector compensation may be somewhat higher in Alberta than in other provinces, the compensation is comparable to that of the private sector with which the public sector competes for workers. In addition, recent settlements with the public sector workers provide modest increases (three years of zero wage increases for teachers).

In summary, the expected revenue gap is large in comparison to provincial spending, provincial expenditures per capita are mid-range among the provinces, those expenditures are now lower relative to personal incomes than during the Klein cuts, and public sector wage settlements are not stressing the budget. Overall, it appears that the province has limited room to reduce public expenditures (at least for a prolonged period).

Higher taxes?

Albertans may look to generating more revenue — that is, raising taxes. Thanks to substantial but unreliable natural resource revenues, Alberta has a large tax advantage. Budget 2014 estimated that Albertans pay $11.6 billion less in taxes than they would pay in the next most tax-competitive province (and almost $24 billion less than in the least competitive province). Albertans’ out-of-pocket burden of provincial finances has been decreasing for 15 years. In the late 1990s, revenues excluding natural resource revenue and investment income (taxes, charges, fees, etc.) amounted to 14.25 per cent of household income. In 2013–14 they amounted to 11.9 per cent. That represents a 16.5 per cent drop in the tax burden of Albertans since 2000.

Alberta could raise taxes sufficiently to meet the projected fiscal gaps and still maintain a significant tax advantage over other provinces. Consider the existing sources. Corporate income taxes were still projected to be at an all-time high of $5.7 billion in the second quarter fiscal update. However, these are sensitive to the business cycle and to energy prices in Alberta. Corporate profits and taxes are likely to drop in the near term, and increased rates will not offer short-term (and perhaps not longer-term) relief.

Personal income taxes are expected to generate $11.2 billion this year. Alberta’s single, or “flat,” 10 per cent tax rate has been subject to some criticism, and changes are often seen as a potential source of revenue. For example, making the tax more progressive by applying a 15 per cent marginal rate on incomes over $100,000 might raise $1.7 billion. If the base personal rate were raised to 11 per cent and also a 15 per cent bracket added on incomes over $100,000, an additional $2.25 billion might be realized.

Other taxes generate $4.4 billion, which comes primarily from the education property tax ($1.9 billion), tobacco taxes ($0.93 billion) and liquor taxes ($0.97 billion). Gaming and liquor revenues yield $2.25 billion and various other premiums and fees provide $1.7 billion. Those total about $8.3 billion, so it would require a large increase in those levies to contribute significantly to the revenue shortfall.

Reinstating health insurance premiums has been suggested. They raised about $1 billion annually prior to being terminated in 2009. Today, allowing for population and income growth, their reinstatement might generate $1.3 billion. However, as a fixed amount per family (or individual) with small concessions for low incomes, it was a very regressive tax.

Another option is a sales tax. Unlike the other provinces and the federal government, Alberta does not have a general sales tax. It is the obvious missing item in Alberta’s fiscal toolbox. Although it appears politically treacherous, introducing a provincial harmonized sales tax is administratively simple and fiscally powerful. Each one per cent rate is generally expected to net the province $1 billion after concessions to low-income persons. Thus, a three per cent tax could generate $3 billion, which is probably more revenue than might be expected from increases in any other major tax or subset of taxes outlined.

In conclusion

So, what is Alberta to do? Albertans might wait (with crossed fingers) for a recovery in energy prices. Some recovery is anticipated, but just how much and when is uncertain. Even so, at the comfortable $95 per barrel level, Alberta was running a structural deficit and borrowing money, so the unanticipated $7 billion revenue hole is only part of the problem.

Furthermore, because bitumen royalties (which have become the province’s major source of resource revenue) depend upon profits rather than production, resource revenues are becoming even more volatile and uncertain than in the past. This crisis may be an opportunity for a more complete fiscal reform.

The government’s response can be expected to involve a combination of deficits, spending cuts and revenue increases. If we are experiencing a recession, a year (or two) of deficit could represent sound fiscal management. As for spending and taxes, Alberta appears to have more of a revenue problem than an expenditure problem, although it may take some pain to convince Albertans that additional taxes, and the amount of additional taxes, are necessary. ❚

Melville McMillan is a professor emeritus in the department of economics at the University of Alberta.